A Representative Assessee and An Authorised Representative, New Income Tax Rules 2026

With the introduction of the new Income Tax Rules 2026, there is a growing question around who can be a Representative Assessee and who is an Authorised Representative.

All entities incorporated outside India, a large population of them are either Foreign Portfolio Investors (FPIs), Foreign Direct Investment (FDI) SPVs or Foreign Venture Capital Investment Funds, are required to obtain a Permanent Account Number (PAN) in India prior to investing/dealing in the securities of an Indian entity.

This PAN is obtained in either of two ways. For FPIs, this can be obtained at the point of obtaining a FPI license in India. All other entities would need to go through a somewhat ‘offline’ method where their CPA would assist them to obtain the PAN.

Earlier, the PAN application form would seek information on the Representative Assessee (RA), only where such RA is appointed by the Assessee (essentially the Foreign Entity). With the introduction of the Income Tax Rules 2026; it is mandatory to either appoint a Representative Assessee (RA) or an Authorised Representative (AR) and their details should be included in the PAN application.

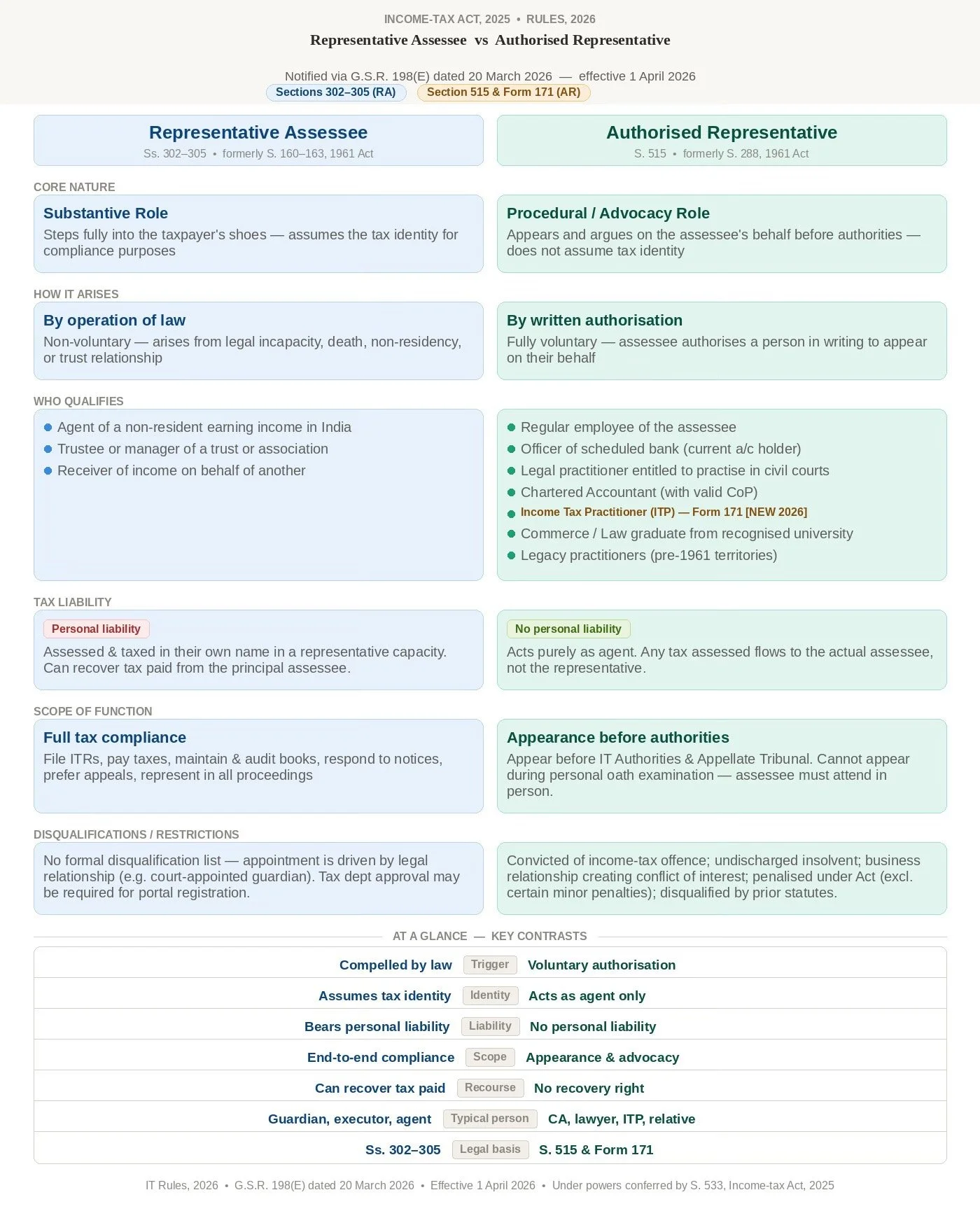

We provide below key differences between RA and AR so that you could make a decision, of which suits your situation better. The broad difference is RA assumes a more substantive role assuming the tax liability of the Assessee; whereas AR is a technical/procedural role more to administratively manage the tax administration efforts for the Assessee.

This brings us to the impact and that is: in addition to the requirement to supply the name, address and contact details of either the RA or the AR, it is now mandatory to also submit Identity and Address proof documents for that RA/AR. Consequently, whereas previously there was no obligation for Category I Foreign Portfolio Investors (FPIs) to provide any identity and address proof for individuals classed as connected parties, the introduction of this new notification means that Category I FPIs will similarly be required to furnish Identity and Address proof documents for their RA or AR going forward.

We hope you found this piece helpful. Please do drop us a comment with your clarifications and inputs. We will review and address your clarifications.

Please note that the above is for informational purposes only and we would recommend that you engage with a CPA in India to know more about the implications of the above on your transactions in India.